The Gold Market in 2026: What Employers Should Know for Their Retirement Plans

Time to read 4 Minutes

Gold has been one of the most talked about investments recently. The price of gold rose significantly in 2025 and has continued to have momentum in 2026, and despite last year’s October pullback, prices have recovered and remain near all-time highs. However, it is important to differentiate between the recent performance of the metal and the historical record of gold’s investment properties.

Why Is Gold in the News?

Gold demand often rises during periods of economic uncertainty, and several factors have contributed to this year’s appreciation:

- Recent Interest Rate Cuts: When interest rates are high, gold, which bears no interest, is comparatively less attractive to interest-bearing bonds. On the flip side, when interest rates are low, interest-bearing bonds become more comparable with gold.

- Tariffs and Trade Policy: Higher import costs and tariff-related inflation expectations have weakened the U.S. dollar, which is notably down this year against major currencies. A weaker dollar typically supports higher gold prices since gold is priced in USD globally.

- Geopolitical Uncertainty: Ongoing global tensions—such as the Russia-Ukraine conflict and trade disputes with China—have added to market volatility, bringing further attention to gold as a perceived refuge for investors.

- Emotion and Sentiment: Gold, which is widely sought for jewelry, has very little industrial use (5%-10%). When prices swing higher, such as they have been, it is often because investment demand has surged and taken the driver’s seat as a proportion of the overall market for gold. These periods are driven increasingly by investor sentiment and emotion making gold prices much more volatile and difficult to predict.1

What Gold Is

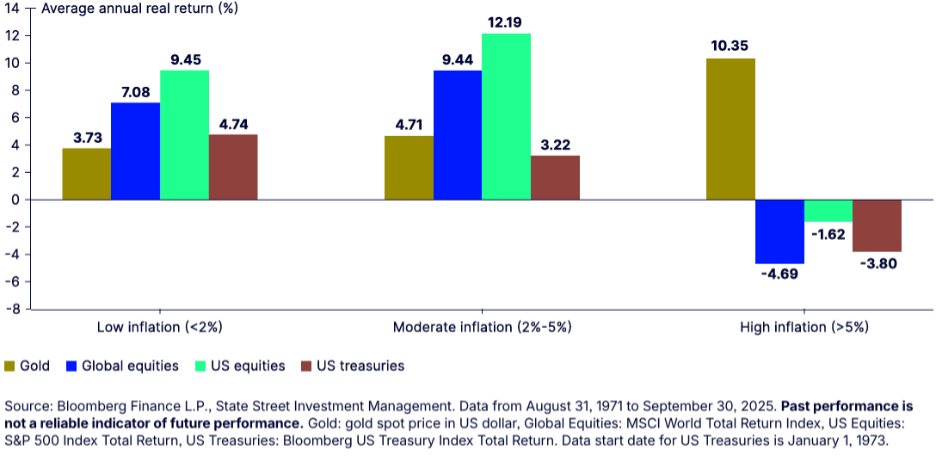

Gold is a hard commodity whose price is determined by its demand. While traditionally viewed as a store of value, this is not a guaranteed hedge for shorter-term inflation but holds more water over a longer-term holding period (See Graph 1 below).

Graph 1: Gold’s Average Annual Rate of Return

Yet there have been extended periods where the metal has underperformed. For example:

- In the 1980s, high interest rates caused gold to underperform for decades. After peaking in 1980, gold took nearly 30 years to exceed that level in nominal terms (See Graph 2) and about 40 years when adjusted for inflation (See Graph 3).

- A bear market from 2011 to 2016 saw gold prices decline by almost half.

Graph 2: Gold Price Historical Chart

Graph 3: Gold Price Adjusted for Inflation

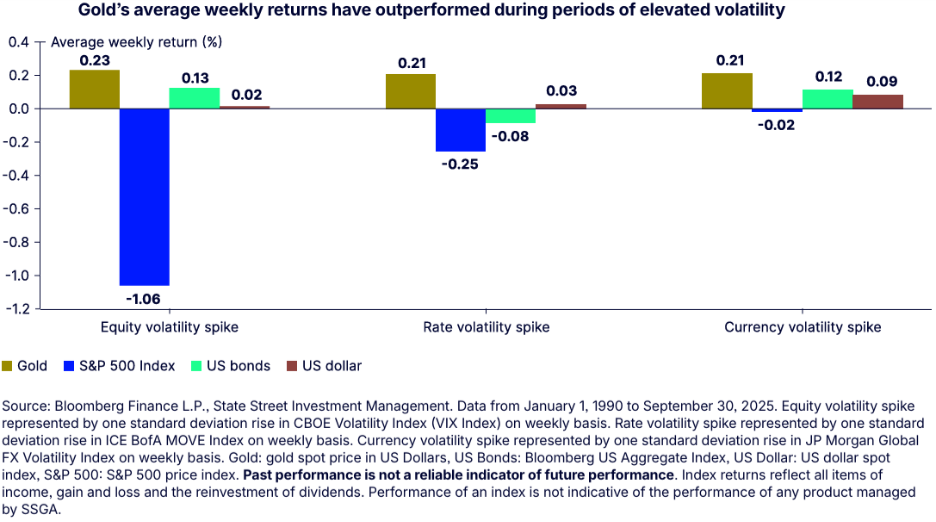

Gold is a potential diversifier for a portfolio.

- Gold generally has a low or negative correlation with equities and has been inversely correlated with real (inflation-adjusted) bond yields (See Graph 4).

- Though in particularly stressful market situations, these relationships may not always hold.

Graph 4: Gold’s Average Weekly Rate of Return

What Gold Is Not

- Gold does not produce income like dividends, interest, or rent. It is an “unproductive” asset.

- It is not a safe driver of portfolio returns. It does not benefit from innovation in the same way that the stock market often does; it also does not directly benefit from economic growth in the way that equities do.

Gold-Related Stocks

Publicly traded gold mining companies are not direct proxies for gold itself as some may suggest. Their performance is shaped by unique cost structures, operational challenges, and geopolitical risks that can impact their performance.

Other Considerations

Gold’s recent rally underscores its role as a potential hedge during uncertainty, but it is not without risk. Investing in gold with the expectation of sustained outperformance can be speculative, especially at current elevated prices. Historically, stocks and bonds have delivered more consistent long-term returns with fewer extended downturns.

What This Means for Your Retirement Plan

Gold’s surge over the past year reflects a unique mix of economic, policy, and geopolitical factors. While it can serve as a potential diversifier in portfolios, it remains subject to volatility and long periods of stagnation. For investors, gold is best viewed as one component of a broader strategy—not a primary driver of returns.

Market movements, including gold’s surge, can leave employers wondering whether their retirement plan investment lineup is prepared for whatever comes next. If you’re looking for a retirement plan advisor who can help your organization navigate volatility with clarity, discipline, and data‑driven guidance, we’re here to help. Contact us today to schedule a consultation.

Learn More About

Investment Guidance

Private Investments and Crypto May Be Available Soon

A new executive order could allow alternative investments like crypto and private investments in retirement plans like 401(k)s and 403(b)s. Learn what this could mean for small and mid-sized companies.

Client Case Study: Reducing Costs Without Sacrificing Performance

An Atlanta-based construction company was experiencing poor returns and high costs for their 401(k) plan under their previous advisor. With the help of Fisher\SMB, they were able to reduce their plan fees while improving their investment quality

How High-Cost, Low-Quality Funds Can Undermine Your Plan

High-cost, under performing funds in your 401(k) plan can erode employee savings and increase fiduciary risk. Learn how partnering with a fiduciary advisor can protect your workforce and strengthen your retirement offering.