How to Use Profit Sharing to Stay “Tax Neutral”

Time to read 3 Minutes

Profit sharing isn’t just a nice bonus—it’s a smart way for business owners to reduce taxes, boost retirement savings, and reward employees. Let’s break it down with a simple example.

The Tax Problem

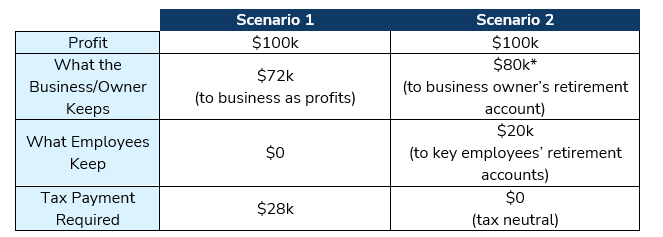

Imagine a 50-year-old woman who owns a successful business. In November, her accountant tells her she made $100,000 in profit this year. Great news, right? Not so fast—she’ll owe $28,000 in taxes. That’s a big check she doesn’t want to write.

So, she uses a 401(k) profit sharing plan to stay help her save tax neutral. Here’s what she does:

- She gives herself a $$80,000 profit sharing contribution (the IRS max for 2026 for someone 50+ and assumes she makes no personal 401(k) contribution).

- She gives $20,000 to a few key employees.

Since profit sharing contributions are 100% tax-deductible, her company’s taxable income drops to $0. That means no tax payment—and the money goes into retirement accounts instead of the IRS’s pocket.

Profit Sharing vs. Paying Taxes

*This is based on a 70-year-old making the maximum profit sharing contribution for 2026. Taxes vary by state. Taxes are deferred until withdrawal at retirement.

For business owners with end-of-year profits, the dollars that would have been lost to taxes can be used to boost an owner’s wealth and help reward and retain key employees.

Why Profit Sharing Is a Win-Win

Using profit sharing for small business owners is a smart move. Here’s why:

- Flexible Contributions

- Your business can decide each year whether to make contributions or not. You can wait until year-end to decide how much to contribute based on your profits. This gives you the flexibility to tailor your profit sharing strategy based on corporate profitability in any given year.

- You Control the Amount

- Unlike a Safe Harbor 401(k), which requires fixed contributions, profit sharing plans let you choose how much to give—and to whom. Contributions can be set up to target specific groups of employees without failing IRS nondiscrimination testing—a win-win for business owners who want to maximize their personal profit sharing without breaking any rules.

- Helps Keep Employees

- You can set a vesting schedule, which means employees earn their retirement money over time. If they leave early, they might lose some of it. That’s a powerful incentive for employees to stay and collect the benefits they earned.

Who Should Use Profit Sharing?

- Business owners with year-end profits

- Companies wanting to reward key employees

- Employers looking for tax-saving strategies

- Teams that want flexible retirement contributions

Let’s Talk

Ready to explore profit sharing at your company? We’re here to help you and your employees navigate the complexities of 401(k) plans and saving for retirement. Contact us to talk about what your business needs.

Learn MOre About

Profit Sharing

Types of Profit Sharing Plans

Profit sharing in a 401(k) helps small businesses reward employees, attract talent, and cut taxes. Learn how it works, types of plans, and how to set it up.

Profit Sharing Guide

Learn how to maximize your retirement plan by implementing a profit sharing plan to reduce plan costs and capture more tax savings.

The Powerful Tax Benefit for Business Owners

Save up to $435,250/year and cut your tax bill—utilizing a powerful combo of Safe Harbor 401(k) and Cash Balance Plan for high-earning business owners. IRS-approved and employee-friendly!