The 4 Levers: How Employers Can Improve Retirement Outcomes

Time to read 3 Minutes

Must-see video

Investment Scorecard

Learn how stronger insights aim to help optimize retirement outcomes for employees and drive better plan decisions. Watch this short 30 second video.

| Visual | Audio |

|---|---|

| A centered “Fisher\SMB” logo appears on a white background, with “Fisher” and “SMB” in dark blue separated by an orange diagonal slash, and a small trademark symbol at the top right. | Music up and under |

| On a white background, large text asks, “How are your plan’s investments really performing?” Beside it, a simple chart shows an upward-trending orange line, with a hand holding a magnifying glass over the graph. | How are the investments in your company’s retirement plan really performing? |

| Two side-by-side gauge graphics appear. On the left, “Your Retirement Plan” shows a question mark. On the right, “Your Industry Peers” displays a number that animates up to 67 within a color-coded gauge. | Our Investment Scorecard gives you an objective view of how your company’s plan compares to industry peers. |

| Understanding these insights can give you an opportunity to boost plan value and employee outcomes. A line chart animates onto the screen, comparing retirement savings over time, with two shaded areas rising across ages 35 to 65 and labeled dollar amounts increasing along the way. | Understanding these insights can give you an opportunity to boost plan value and employee outcomes. |

| The Fisher\SMB logo appears centered above a phone number and the Fisher\SMB website URL displayed side by side on a white background. | See where your company’s plan stands and where you can compete. |

| A solid dark blue screen appears with the following disclosure centered along the bottom: Investing in securities involves the risk of loss. Intended for use by employers considering or sponsoring retirement plans; not for personal use by plan participants. Fisher Retirement Solutions®, Fisher\SMBTM, FisherSMB, and all related logos and designs are trademarks of Fisher Retirement Solutions, LLC, which is not connected to Fisher Investments. ©2026 Fisher Retirement Solutions. K052607MC | Music fades out |

Employers who want to do more to help employees retire comfortably have four levers they can pull to improve their retirement plan:

- Reduce fees

- Increase employer match

- Encourage employee contributions

- Improve investment returns

Some employers might tackle all four at once, but if you can only choose one, which should you choose? Here’s what we found out.

Investigating Your Options

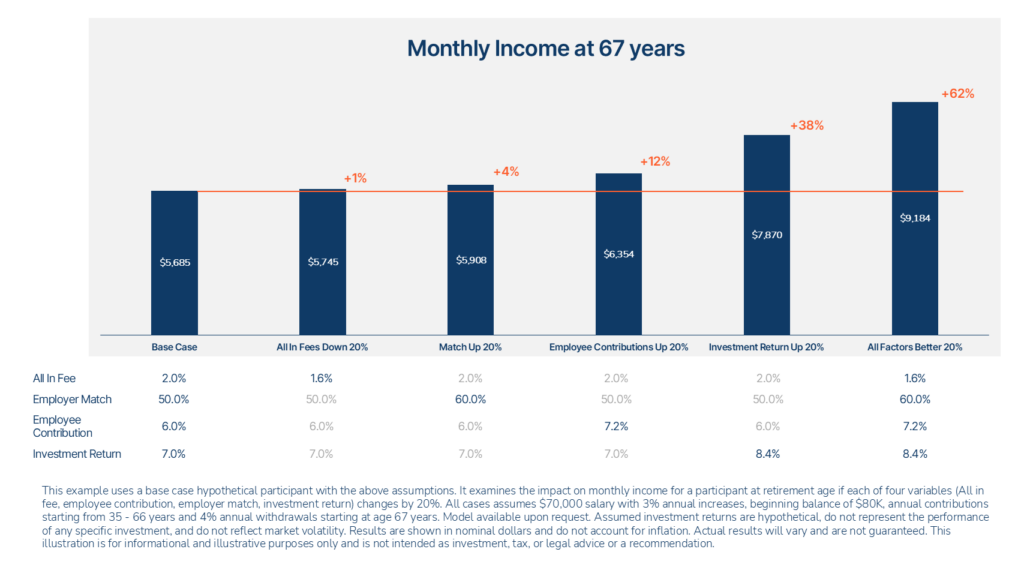

To determine which lever delivered the best ROI, we created a hypothetical scenario for an employee who is 35 and makes $70,000 per year. We assumed a baseline of 2% fees, 50% employer match, 6% employee contribution, and 7% investment returns. We then asked: If we improved each of these levers individually by 20%, which one would yield the most monthly income at age 67?

- Fees: Lowering fees by 20% reduced them to 1.6%. That’s good but it only increases monthly income by 1%.

- Match: Increasing the employer match to 60% was better but still only delivered a 4% improvement.

- Employee contributions: This is where we start to see meaningful increases. Bumping up contributions to 7.2% jumped the monthly income by 12%—nearly $700 per month.

- Investment returns: Now the gains are getting big. A 20% increase in returns to 8.4% leads to a monthly income increase of 38%. That’s $2,185 per month!

Clearly, if you can only do one, increasing investment returns offers the most bang for your buck, but we went a step further. What if an employer did pull all four levers at once?

It turns out, each lever boosts the others so that the cumulative effect is greater than the sum of each part. Increasing all four factors by 20% leads to a 62% increase in monthly income—that’s $3,499 more per month.

But How Do Employers Affect Investment Returns?

You don’t control the markets but you can influence investment returns through the lineup of funds you make available in your plan. If your plan is stuffed with low-quality, underperforming funds, employees lose out on potential returns. However, if you and your advisor work together to include funds that consistently perform above the median, employees can earn a lot more over time.

To maintain a high-quality fund lineup:

- Benchmark the funds every few years. If there are funds performing below the median, consider replacing them with funds that have a more consistent track record of success.

- Look for conflicts of interest. You may be able to see revenue sharing in fee disclosures. Or you can simply ask your advisor if anyone is paying them to make referrals.

- Work with a fiduciary advisor. Simply by hiring a fee-only advisor who’s legally obligated to put client interests first, you can help your employees boost their returns.1 2

Not all retirement plans are built the same and not all plan investments offer the same value. By focusing on what helps employees maximize their returns, you can make a significant difference in the quality of your employees’ retirement.

See How Your Plan’s Investments Stacks Up

Compare your investment lineup against similar plans using objective data. Download the Investment Scorecard to see whether your plan’s investments are pulling their weight.

learn more about

Plan Optimization

Understand Safe Harbor Contribution Options

This chart explains the three Safe Harbor contribution methods, Basic Match, Enhanced Match, and Non-Elective so you can see how employer contributions work and what they mean for compliance and employee benefits.

3 Common Retirement Plan Mistakes to Avoid

Avoid 3 common retirement plan mistakes: choosing the wrong plan, skipping a specialist advisor, and waiting too long to start. Learn how to save more, reduce taxes, and take advantage of valuable 401(k) tax credits for your business and employees.

Tax Treatment Table of Retirement Accounts

How Different Retirement Accounts Are Taxed: From Roth IRAs to 401(k)s and Mega Backdoor Roth strategies, this table breaks down contribution limits, tax treatment, and withdrawal rules, helping you choose the right mix for your retirement savings.