12 Essential Cash Balance Plan Questions

Time to read 5 Minutes

12 Essential Cash Balance Plan Questions for Business Owners

If you’re a business owner with steady profits and you’re looking for smart ways to save more for retirement and cut down on taxes, you might want to take a closer look at cash balance plans. These plans can be a game-changer when paired with your company’s 401(k), but they’re not for everyone. So, what exactly is a cash balance plan—and is it right for your business?

Let’s break it down with 12 essential questions (and answers!) to help you decide if this powerful retirement strategy is worth exploring.

1. What’s a Cash Balance Plan, Anyway?

Think of a cash balance plan as a hybrid between a traditional pension and a 401(k). It’s technically a defined benefit plan, but it feels more like a Traditional 401(k) because it shows a “cash balance” that grows every year. Your business makes fixed contributions, and employees (including you!) get a guaranteed amount at retirement.

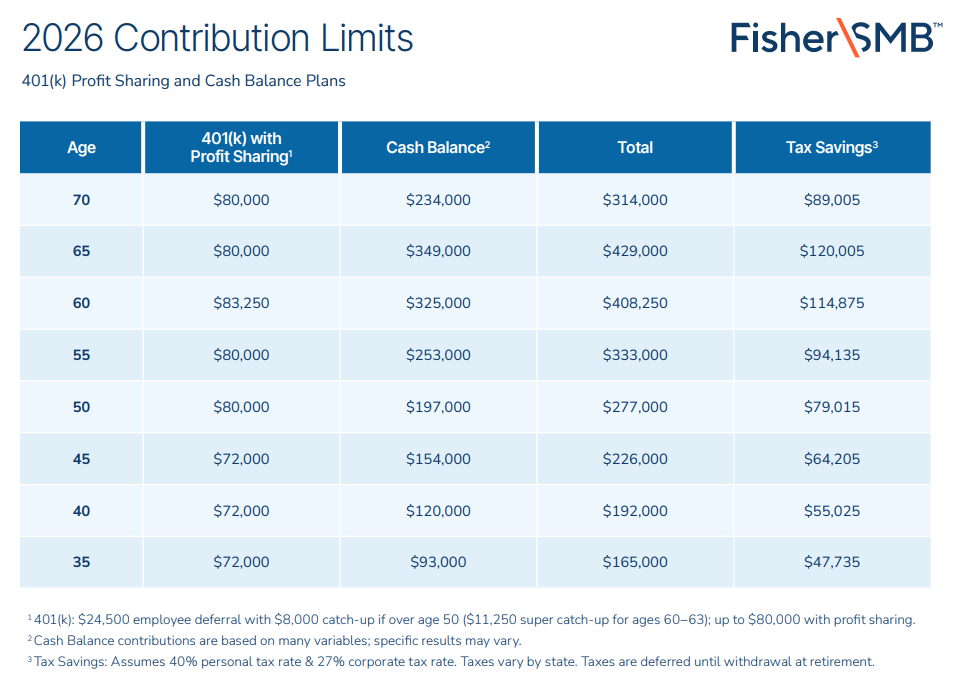

2. Why Should I Care?

Because it can save you a ton in taxes and help you stash away more for retirement than a 401(k) alone. In 2026, the max you can put into a 401(k) with profit sharing is $72,000 (or $80,000if you’re 50+). But with a cash balance plan? You could contribute up to $359,000 depending on your age. That’s a massive boost to your retirement savings—and a big tax deduction for your business.

3. How Do Cash Balance Plans Work?

Each participant has a “hypothetical” account that grows every year with two components:

- A pay credit (a percentage of salary or a flat dollar amount)

- An interest credit (either a fixed rate or tied to an index)

Even though the account isn’t like a regular investment account, it feels familiar to employees because it shows a clear balance that grows over time.

4. Can I Have a 401(k) and a Cash Balance Plan?

Yes! In fact, combining both is a popular strategy. You can max out your 401(k) and profit-sharing contributions, then stack a cash balance plan on top for even more savings.

When it comes to retirement plans, cash balance plans and 401(k)s play by different rules. Here’s a quick breakdown:

- Who Pays In: With a cash balance plan, the company foots the bill—employees don’t contribute. In a 401(k), employees usually chip in, and employers might match a portion.

- Who Takes the Risk: In a cash balance plan, the employer takes on the investment risk. In a 401(k), it’s all on the employee—your returns depend on how your investments perform.

- Payout Options: Cash balance plans can offer lifetime annuities (think steady paycheck in retirement). Most 401(k)s don’t.

- Safety Net: Cash balance plans are usually backed by the PBGC (a federal insurance program). 401(k)s don’t have that kind of protection.

5. Who’s a Good Fit for a Cash Balance Plan?

Cash balance plans are ideal for:

- Business owners over 40

- High earners (think $275K+ annually)

- Companies with steady profits

- Firms with fewer than 15 employees per owner

- Owners who want to catch up on retirement savings fast

6.What Are the Tax Perks of having a Cash Balance Plan?

Contributions are tax-deductible for your business and grow tax-deferred. That means you lower your taxable income now and build wealth for later. Win-win.

7. What’s the Catch?

Cash balance plans are more complex and require annual contributions. You’ll need to commit to funding the plan each year. You might also consider getting help from a pro—like an actuary or retirement plan specialist—to keep everything running smoothly.

8.What About My Employees?

You’ll need to include a portion of your team, as the IRS requires plans not to disproportionately benefit HCEs compared to NHCEs. For example, you might contribute a flat rate for yourself and just a percentage of salary for other employees, as long as it passes IRS testing.

Did you know you can add a Safe Harbor component to automatically pass most IRS compliance tests? Learn more here.

9.What If the Market Tanks?

Here’s the deal: your business guarantees a certain return (the interest credit), so if the market underperforms, you’re on the hook to make up the difference. But if the market does well, your required contribution could go down. It’s a balancing act, but manageable with the right investment strategy.

10. Can I Change or Stop the Plan?

Cash balance plans are meant to be long-term, but they can be amended or even terminated if needed. Just know that it’s not something you want to start unless you’re ready to stick with it for a while.

11. Where Does the Money Come From?

All contributions come from your business—not your employees. But here’s the cool part: you can use those contributions to reduce your personal taxable income. For example, a doctor earning $500K might take $150K as a cash balance contribution instead of salary, cutting their tax bill significantly. You can read the case study below.

12. What Should I Think About Before Adding a Cash Balance Plan?

Before you dive in, consider:

- Can your business commit to annual contributions?

- Are you okay with higher admin costs and complexity?

- Do you have a trusted advisor or actuary to help manage the plan?

If the answer is yes, a cash balance plan could be a powerful addition to your retirement strategy.

Cash balance plans aren’t for everyone, but if you’re a successful business owner looking to save more and pay less in taxes, they’re definitely worth a look. With the right setup, you can build serious retirement wealth while keeping more of your hard-earned money today.

Let’s Talk

Want to see if a cash balance plan makes sense for your business? Contact us to talk to a Fisher\SMB Business Specialist about your company’s needs.

Learn More About

Cash Balance Plans

Cash Balance 101

Cash balance plans can turn taxes into wealth. This powerful tax strategy can help you convert more of your company’s hard-earned profits into retirement savings.

Cash Balance Case Study

Check out how a high-earning doctor, who’s both a business owner and employer, can use this IRS-sanctioned strategy to reduce her tax bill by more than $100k a year.

Cash Balance Guide

What you need to know to unlock huge savings is right here, from the benefits of this type of plan to the challenges of building and maintaining a Cash Balance plan over time.