3 Ways Your 403(b) Could be Costing You Big

Thank You

Click the button below to begin your download, please contact us if you have any questions.

A 403(b) plan for their now, later, and after.

You’ve crafted something real. Not just a nonprofit, but a culture. That’s why we approach serving your employees like their future depends on it, because it does.

What is a 403(b) Plan?

A 403(b) Plan is a type of retirement plan for the employees of certain nonprofit organizations like schools, hospitals, charities, and churches.

How it Works

Similar to a 401(k) plan, a 403(b) plan allows employees to save a percentage of their salary, tax-deferred, and invest that money for retirement.

How a 403(b) is Different

A 403(b) is different than a 401(k) in some ways, including investment options and some administration processes.

How Fisher\SMB™ Can Help

As a fiduciary advisor, Fisher\SMB helps nonprofits navigate, evaluate, and set up a 403(b) tailored to their objectives.

Downloadable Chart

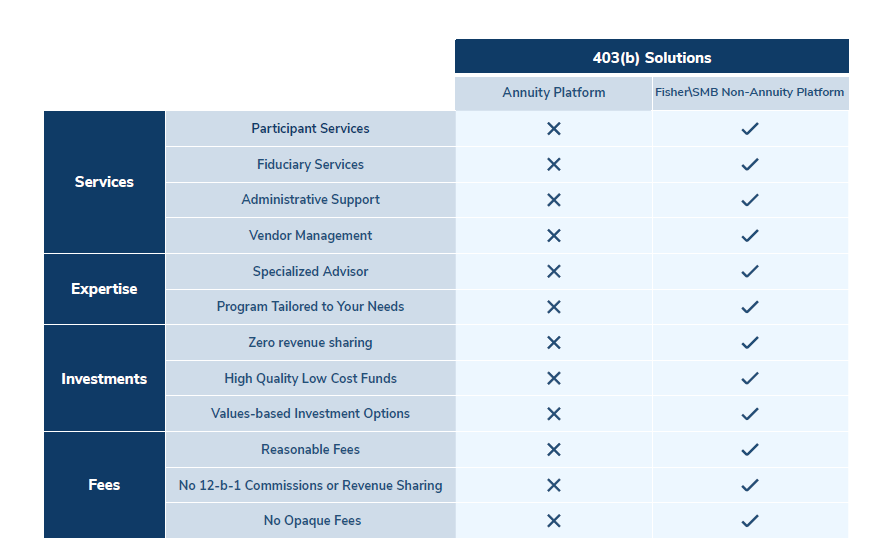

Compare 403(b) Solutions

There are two main types of 403(b) solutions: annuity-based or non-annuity-based. While annuity 403(b) plans can provide guaranteed returns and income options to help protect against outliving savings, they be problematic to your employees in three critical areas: fees, investment quality, and service.

Case Study

Plan Participant

See how an employee can benefit when an employer moves from an annuity-based to a non-annuity-based 403(b) solution.

downloadable GUIDE

Your 403(b) Can Cost You Big

More than half of all 403(b) retirement plans are on an annuity platform, which is an outdated system that could be charging participants higher fees. Download our complimentary guide to learn the three ways annuity plans can be problematic for employees.

What’s the Difference Between a 401(k) and 403(b) Plan

401(k) and 403(b) plans both help employees save for retirement, but differ in eligibility, compliance, and investment options. This guide helps business and nonprofit leaders choose the right plan for their team and goals.

See What Our Clients Have to Say

- Testimonials are representative of client views at the time collected. Clients are not compensated financially or otherwise for testimonials. There are no known material conflicts of interest between the client and Fisher\SMB that could influence the testimonial content.

Contact Us

One of our retirement specialists would love to talk to you about your company’s retirement plan needs.

Call Us

(844) 238-1247