What Is Financial Wellness, Really?

Time to read 4 Minutes

A holistic look at budgeting, saving, debt, and retirement

Financial wellness is one of those terms that can mean different things to different people. But at its core, it’s about having a positive and secure relationship with money. It’s not just about being debt-free or having a retirement account; it’s about feeling in control, prepared for the unexpected, and confident about the future.

A truly holistic approach to financial wellness includes budgeting, saving, managing debt, and planning for retirement. It also includes having an emergency fund, which can provide peace of mind and a buffer against life’s surprises. Many people find their money being pulled in multiple directions, often without a clear understanding of where it’s going each month. That’s why building a thoughtful, realistic plan is so important.

Beyond the Basics: More Than Just Debt-Free

While minimizing debt is certainly a goal, financial wellness goes deeper. It’s about creating space to make intentional financial decisions. Carrying high-interest debt can limit flexibility and delay progress toward other goals. Reducing or eliminating that debt can open the door to more meaningful conversations about saving, investing, and planning for the future.

Still, it’s important to recognize that paying off debt—while beneficial—can sometimes feel like a roadblock to doing anything else. That’s why a balanced approach is key.

Budgeting: The Foundation of Financial Wellness

Budgeting is often the first step toward financial wellness, but it’s also one of the most misunderstood. Many people create a budget quickly, only to find it doesn’t reflect their actual spending habits. A good budget requires a deeper dive—one that accounts for both fixed expenses and discretionary spending, as well as those unpredictable one-off costs that always seem to pop up.

The biggest challenge isn’t creating the budget—it’s sticking to it.

Discipline plays a major role, and so does flexibility. A budget should be a living document, not a rigid set of rules. When done right, it becomes a powerful tool for making informed decisions and reducing financial stress.

Balancing Today and Tomorrow

One of the most common challenges people face is figuring out how to save for both short-term and long-term goals. It’s not easy, and there’s no one-size-fits-all answer. The key is to start with personal financial goals and build from there.

Establishing an emergency fund is often a top priority. It provides a sense of security and helps prevent setbacks when unexpected expenses arise. Start with saving $1,000 in a bank savings account. After that, work toward 3 – 6 months of living expenses saved. Another top priority is your retirement savings, especially if your employer offers a 401(k) match. Contributing at least enough to receive the full match is a smart move, as it’s essentially free money.

Once those foundations are in place, the focus can turn to debt repayment. This progression allows for greater financial flexibility over time. Of course, it requires sacrifice. Delayed gratification—choosing to save for retirement instead of spending impulsively—can make a significant difference in the long run.

Debt: A Tool or a Trap?

Debt plays a complicated role in financial wellness. While it’s often viewed negatively, it can be used strategically in certain situations, particularly in low-interest environments. The key is having a clear plan and the discipline to follow it.

Many people rely on credit cards when cash is tight, but this can quickly spiral if balances aren’t paid off regularly. Shifting back to debit cards and using interest-free balance transfers can be effective strategies for managing debt. Still, the most important factor is mindset. Debt should be approached with caution and a plan—not as a default option.

Signs of Financial Wellness (Even Without Wealth)

Financial wellness doesn’t require a six-figure salary or a luxury lifestyle. In fact, many people who feel financially well don’t consider themselves wealthy. They may live below their means, avoid high-interest debt, and contribute regularly to retirement savings—even if it’s a small amount.

Emotional well-being is also a key indicator. Lower financial stress often correlates with lower debt and better money management. Being in tune with financial tools and resources (like our Retirement Calculator and Budgeting Worksheet), and making informed decisions, are strong signs of wellness—even if the numbers don’t look flashy.

Focus on Your Own Journey

Perhaps the most important takeaway is that financial wellness is personal. There’s no universal formula, and comparisons to others can be misleading. Just because someone drives a nice car doesn’t mean they’re financially well—you don’t know how they paid for it.

The best approach is to focus inward. Set goals that align with your values and circumstances. Progress may be slow at times, but every step forward counts. Financial wellness isn’t about being perfect; it’s about being intentional, informed, and in control

Your Fisher\SMB retirement specialists can help you understand your financial wellness situation, create personalized goals, and develop an action plan to reach them. Contact us at 888-322-7586 or contact401k@frs.net today!

Learn MOre About

Personal Financial Wellness

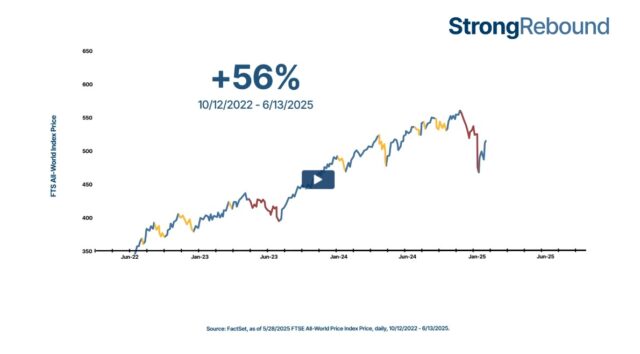

Market Update

Q2 was a tale of two halves—tariff tensions hit early, but markets found their footing. After a shaky start, market sentiment turned positive. Watch the video to learn more.

Money Minute

This 2-minute video breaks down essential concepts like mutual funds, compound growth, and contribution limits—so you can make smarter financial decisions

Social Security Optimization Strategies

Social Security is an important part of retirement, but making the most of it takes some planning. Read the article to learn more.