Social Security Optimization Strategies

Time to read 5 Minutes

When to claim and how it fits into your retirement plan

For many Americans, Social Security is a foundational piece of retirement income. But deciding when and how to claim benefits isn’t always straightforward. The right strategy depends on a mix of personal factors—like health, income needs, and family longevity—as well as a clear understanding of how the system works.

Here’s a breakdown of key considerations to help you make informed decisions about Social Security and how it fits into your broader retirement plan.

Understanding Your Claiming Age

The first step in optimizing Social Security is understanding the impact of timing. Benefits can be claimed as early as age 62, but doing so comes with a trade-off. Claiming before the full retirement age (FRA)—which is 67 for those born in 1960 or later—results in a permanent reduction in monthly benefits. For example, someone who claims at 62 will receive only about 70% of their full benefit1.

On the flipside, delaying benefits past the FRA increases monthly payments. For each year benefits are delayed up to age 70, the monthly amount grows by approximately 8%. This can be a powerful strategy for those in good health or with a family history of longevity.

How Benefits Are Calculated

Social Security benefits are based on your highest 35 years of earnings, adjusted for inflation. If you haven’t worked for 35 years, the missing years are counted as zero, which can lower your benefit. That’s why continuing to work, especially in higher-earning years, can increase your future payments.

You can get a personalized estimate of their benefits by creating a “my Social Security” account at ssa.gov/myaccount. This tool provides a detailed look at projected benefits based on different claiming ages and earnings scenarios.

Social Security’s Role in a Retirement Plan

Social Security is designed to cover basic living expenses in retirement, not to replace full income. That’s where a 401(k), 403(b), or other retirement savings plan comes in. Think of Social Security as the foundation—covering essentials like housing, food, and healthcare—while personal savings support discretionary spending and lifestyle goals.

When Delaying Makes Sense (and When It Doesn’t)

Delaying Social Security can be especially beneficial for those who:

- Are still working and earning a high income

- Want to replace lower-earning years in their 35-year average

- Are in good health and expect to live well into their 80s or beyond

- Have other income sources to rely on in the meantime

However, delaying may not be ideal for everyone. Those with health concerns, shorter life expectancy, or immediate income needs may benefit from claiming earlier. It’s also important to consider the break-even point—the age at which the total value of delayed benefits surpasses the value of claiming early. For many, this occurs in their late 70s.

Spousal and Survivor Benefits

Spousal and survivor benefits add another layer of complexity—and opportunity. A lower-earning spouse may be eligible for up to 50% of their partner’s benefit, even if they never worked. In the event of a spouse’s death, the surviving partner may receive up to 100% of the deceased’s benefit, depending on their personal earnings and claiming age.1

Divorced individuals may also qualify for spousal benefits if the marriage lasted at least 10 years and they remain unmarried. These benefits don’t reduce the ex-spouse’s payments and can be a valuable source of income for those who qualify.

Health, Longevity, and Employment Status

Personal health and family longevity are major factors in the claiming decision. Those in good health with a family history of long life may benefit from waiting, while those with chronic conditions or shorter life expectancy may prioritize earlier access.

Employment status also matters. Continuing to work past 62 can reduce benefits temporarily if earnings exceed the annual limit, but it can also boost future payments by increasing lifetime earnings averages.

Common Misconceptions

Despite its importance, Social Security is often misunderstood. Here are some of the most common misconceptions you should be aware of:

- Confusing early eligibility with full retirement age: Many assume they receive full benefits at 62, but full retirement age is typically 67 for those born in 1960 or later.

- Assuming Medicare and Social Security are linked: While Medicare eligibility begins at 65, it operates independently of when you claim Social Security benefits (FRA of 67).

- Overlooking spousal or survivor benefits: Lower-earning spouses, including divorced individuals, may be entitled to a portion of their partner’s benefits, but many don’t realize it.

- Leaving money on the table: A significant number of people don’t receive the full benefits they’re eligible for due to a lack of understanding about the options available to them.

Advice for Younger Workers

Younger workers often worry that Social Security won’t be around when they retire. While the system does face funding challenges, it’s unlikely to disappear. According to the Social Security Administration (SSA), even if no changes are made, payroll taxes will still cover about 80% of scheduled benefits after 2035.1

That said, younger participants should plan as if Social Security will be a bonus, not a backbone. Building a strong retirement plan is the best way to ensure financial independence in retirement.

Social Security Requires Planning

Social Security is a valuable benefit, but optimizing it requires planning. The right strategy depends on personal goals, health, income needs, and family dynamics. By understanding the rules and using available tools, you can make informed decisions that support a more secure retirement.

Our retirement specialists can help you understand your Social Security situation, your options, and how it fits into your overall retirement planning and goals. Contact us at 888-322-7586 or contact401k@frs.net today!

Learn More about

Personal Financial Wellness

Market Update

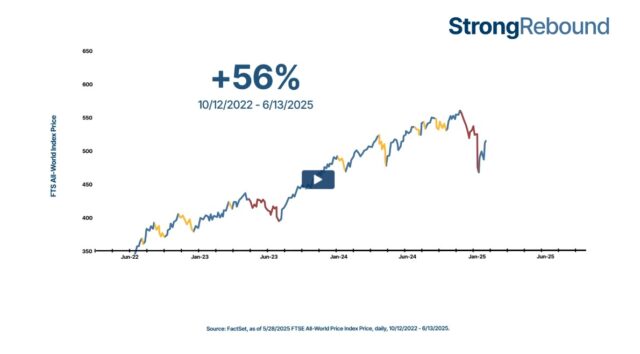

Q2 was a tale of two halves—tariff tensions hit early, but markets found their footing. After a shaky start, market sentiment turned positive. Watch this short video to learn more.

Financial Wellness

Financial wellness is more than being debt-free. It’s about having a plan, being ready for surprises, and making smart choices. Even if money’s tight, you can still be financially “well.” Read the article to learn more.

Money Minute

This 2-minute video breaks down essential concepts like mutual funds, compound growth, and contribution limits—so you can make smarter financial decisions